TAX • 19 SEPTEMBER 2023 • 4 MIN READ

How do VAT penalties work?

If you regularly deal with VAT (Value Added Tax), the new VAT Penalty regime is essential to understand. This article covers how VAT penalties work, certain exemptions, and how to avoid these penalties.

VAT accounting periods can be monthly, quarterly, or annually, depending on how often you need to report your VAT transactions. The deadline to submit VAT returns to HMRC is one month and seven days after the end of your VAT accounting period. For example, if your VAT period runs through the 1st of January to the 31st of March quarter, you have until the 7th of May to submit your return.

The VAT payment due date is usually the same as the submission deadline. If you've set up a direct debit, HMRC will collect the payment three working days after the submission deadline, meaning you won't have to worry about making manual payments.

Before the 1st of January 2023, late submission VAT penalties were processed through a more complicated system. With the new points-based system, things are much simpler. Here’s how it works:

Each time you submit your VAT return late (even if it's a nil or repayment return), you'll receive a penalty point. When you reach a specific amount of these points, HMRC will charge you a £200 penalty. If you continue to submit late while you're already in the penalty zone, there'll be an additional £200 penalty for each subsequent late submission.

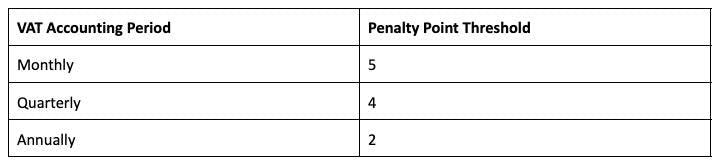

The penalty point threshold depends on your VAT accounting period and how frequently you file VAT returns:

Exemptions to VAT penalties

The following VAT returns are exempt from the late submission penalty rules:

- The first VAT return after you register for VAT

- The final return after you cancel your VAT registration

- One-off returns that cover a period other than a month, quarter or year (for instance, a 4-month period after a switch from a quarterly VAT accounting to annually).

Got any questions about Beany?

Chat to one of our friendly team today to get clarity.

Removing penalty points

As long as you haven’t reached the penalty point threshold, a penalty point will expire on the last day of the month 24 months after the VAT submission deadline.

For example, for the 1st of January to the 31st of March 2022 quarterly period, the submission deadline is on the 7th of May 2023. A late submission penalty point from this period would expire on the 31st of May 2025.

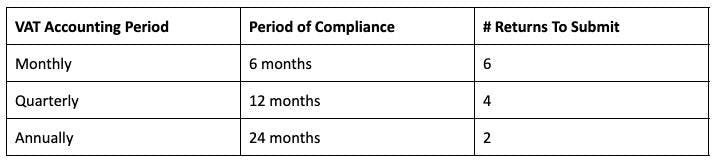

If you’ve reached the penalty point threshold for your VAT accounting period and wish to remove your penalty points, you must meet two conditions:

- Complete a period of compliance by submitting all VAT returns by their deadlines

- Submit all outstanding VAT returns for the previous 12 months

The period of compliance generally starts on the first of the month following the missed submission deadline. For instance, if the submission deadline was the 7th of May, the period of compliance would start on the 1st of June.

VAT late payment penalties

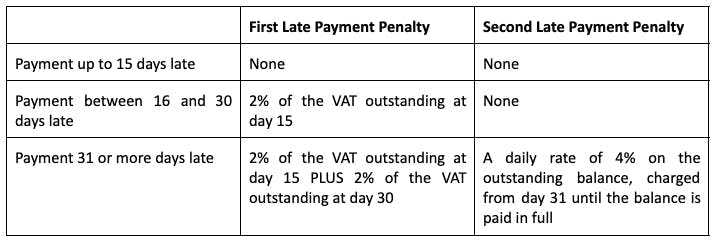

VAT late payment penalties are issued when you don't pay your VAT liabilities and penalties by the due date.

If your payment is 16 days late, you’ll receive your first penalty. Once your payment is late for 31 days or more, you’ll be issued a second penalty, along with an increase on the first penalty. Make sure to mark your VAT due dates on your calendar!

Below is a breakdown of the late payment penalties:

Exemptions

Some VAT payments are exempt from the late payment penalties, including:

- VAT payments on account

- Instalments for the VAT Annual Accounting Scheme

Period of familiarisation

HMRC will not be charging a first late payment penalty until after the 31st of December 2023 (subject to some conditions), giving business owners time to adapt to these changes.

Late payment interest

HMRC will charge late payment interest from the first day your payment is overdue until the day it is paid in full. This interest is charged on late payment of VAT liabilities, overdue late submission penalties, and overdue late payment penalties.

Late payment interest is charged at the Bank of England base rate, plus 2.5%.

Time to pay arrangements

To reduce your chances of receiving VAT penalties, it’s important to contact HMRC as soon as you realise you can’t pay your VAT on time - don’t wait until the payment deadline.

The HMRC may propose a ‘Time to Pay’ arrangement, a flexible plan adapted to the financial circumstances of your business.

If you do agree to a Time to Pay arrangement with HMRC, you need to make the agreed payments on time. Failure to do so may result in cancellation of the arrangement, and reinstatement of late payment penalties.

Simply put, the best way to avoid penalties and interest is to submit and pay your VAT returns on time. Beany can help you stay on top of these payments and deadlines - reach out to us to get started.

Who are Beany?

We’re an online accounting firm that is always right here for you, your accounting pain relief. The most advanced technology lets us work way more closely with you than a normal accountant world.

We have a dedicated team of certified accountants and a support team to take care of your business no matter where you are, so you can focus on growing your business. We take out the ‘fluff’, break down the barriers and get things done. Looking out for you is what we are all about. Get started for free today.

Kate Eastman

Senior accountant

Certified Chartered Accountant and Tax Adviser based in Surrey. I love cheese, chips, chocolate and coastal walks. I dislike horror movies, seafood and traffic jams.

subscribe + learn

Beany Resources delivered straight to your inbox.

Beany Resources delivered straight to your inbox.

Share:

Related resources

VAT guide for UK business owners

April, 2025Value Added Tax (VAT) is a tax on most goods and services sold by businesses.

How (and when) to register for VAT

October, 2022VAT is a tax on most goods and services in the UK. How does VAT work? When should you register or deregister?

10 common VAT mistakes small business owners should avoid

May, 2024VAT can be tricky if you don’t deal with it on a daily basis. Fixing these mistakes can be expensive, so we’ve comp...