NEW BUSINESS • 14 SEPTEMBER 2022 • 10 MIN READ

9 things to ask your accountant when starting a small business

According to the Australian Bureau of Statistics, there was a 7.0% or 167,646 increase in the number of businesses on 30 June 2022 compared to the previous year. Starting your own small business is exciting; you don’t have to work the 9-5, can be your own boss and can create your own schedule. However, it’s not easy. You have to think about how to operate your business, sales and marketing plans, bookkeeping and filing tax returns and so much more. You will wear many hats!

Seeking professional advice can help you set up and kick start your small business smoothly while you can focus on the aspects of your business that are an effective use of your time - hopefully driving revenue!

In this blog, we’ll discuss 9 things you should ask your accountant when starting a small business. From “How should I structure my small business?”, “How should I finance my small business?” to “What happens if I want to exit my small business?”; having these discussions will help both you and your accountant understand how to set yourself up for success and achieve your goals.

1. Should I hire an accountant before starting a small business?

Many business owners hesitate to hire an accountant before starting a business or in the startup phase because of the cost. However, accountants do more than file taxes and keep books. An experienced accountant acts as a business advisor for small businesses. From setting up financial goals, establishing a financial system, maintaining compliance, and providing guidance based on your business's financial performance, they can assist you with navigating the financial aspects of your business. They can also ensure that you are claiming all the deductions you can and in particular any eligible pre-setup costs.

2. How should I structure my business?

One of the most important decisions to make when starting a small business is to choose a business structure that suits you.

Should your business be set up as a sole trader, partnership, company, or trust? What are the advantages and disadvantages of these structures? How does the business structure impact my tax obligations? How much time and costs are involved in setting up the business structure that suits you? How much control do you want to have in your business? What about asset protection and fundraising? What if you want to exit your business in the future?

You should carefully consider these factors when choosing a business structure. No matter how you decide to proceed, an accountant can assist you in weighing your options and mitigating risks.

3. How should I finance my small business?

Some common ways to finance your small business are using your own savings (referred to as bootstrapping), borrowing money against your equity or taking on debt from a bank, borrowing from family or friends and taking advantage of government grants and crowdfunding.

The best way to finance your small business depends on your circumstances, but an accountant can assist you in weighing the pros and cons of your options. For example, if you can do so, bootstrapping is likely the most straightforward way to start a business and ensure that you retain full ownership. However, you should keep your overhead costs at a minimum especially when you’re just starting out. Although you'll give up some of your shares if you decide to go down the equity financing route, you'll receive a capital investment that can be used for marketing, R&D, payroll, product development and more.

4. How should I keep my books?

It’s recommended by Beany accountants that you should keep your business bank account separate from your personal one. In fact, you really need 2 - one separate business account for your normal business trading transactions and the other for your tax savings.

If you’re GST registered, putting aside 10% of your gross sales will ensure that you always have sufficient funds to pay your GST. On top of that, you should also put aside funds to cover your income tax - the amount depends on how much you earn, but some indicative figures based on the 2022-2023 tax rates would be:

- 15% of your profit if you earn/make a profit of $50,000

- 22% of your profit if you earn/make a profit of $75,000

- 25% of your profit if you earn/make a profit of $100,000, or if you are trading through a company turning over less than $50m annually

If you are registered for GST, your BAS will show you a fixed PAYG tax amount (monthly or quarterly depending on your turnover) that is calculated off your estimated income for the year so you will know what tax amount to put away for.

You can discuss your specific situation with your accountant to decide on an appropriate figure for your business. This will then ensure you have enough money to pay the ATO at tax time.

5. What records should I keep?

As a small business owner, you should keep detailed records of all transactions. These include:

- Statements for your bank and/or credit card accounts

- Copies of all your sales invoices

- Copies of all your receipts for purchases or expenses

- Calculations of the figures entered onto your BAS

- Company constitutions

- Trust deeds

- Share Registers if applicable

- Annual financial reports

There are also a number of legal documents that you need to keep, such as employment contracts, contracts with suppliers or trading partners; a lawyer can advise you on this.

Nowadays the ATO will accept electronic copies of most documents, so these can be saved electronically using Xero Files, HubDoc, Receipt Bank or Google Drive. In most cases, you’re required to keep these records for 5 years from the date you lodge the relevant tax return.

For more detailed guidelines on record keeping, visit ATO’s website.

6. Do I need to register for GST?

If your business’s turnover exceeds $75,000 per year, or you expect it to exceed this threshold in the next year, then you will need to register for GST. You can also choose to be GST registered voluntarily, even though you earn under $75,000; you may wish to do this for one of the following reasons:

- If you only sell to businesses that are themselves GST registered, it will make no difference to them if you charge GST as they can reclaim it. You can therefore effectively increase your sales by 10% without affecting your customers, and be able to claim back the GST on your own purchases

- GST can be claimed back on the business assets you purchased to set the business up

- If the items you sell are GST-Free (for example, food ingredients, education courses, some medical items), you can claim back GST on your purchases without having to charge GST on your sales

- If eligible, you will need to register for GST if you wish to claim Fuel Tax Credits

If you want or need to register for GST, simply follow these steps on ATO’s website or you can let your Beany accountant handle this.

7. What are my tax obligations?

Your tax obligations will vary according to your business type, the number of employees and the fringe benefits you offer your employees.

Sole trader

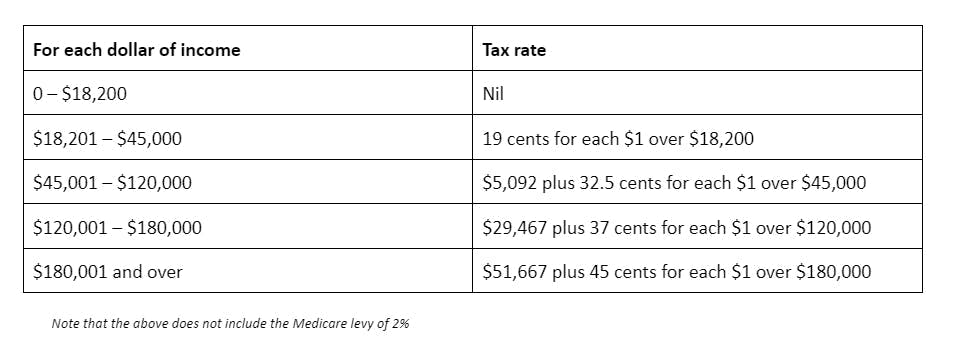

A sole trader business structure is taxed as part of their own personal income. This means sole traders are taxed at Individual Income Tax Rates and entitled to a tax-Free threshold of $18,200. From 1 July 2022, individual tax rates are below:

At the end of the financial year, sole traders must lodge an individual tax return by 31 October each year unless you register with a tax agent before the 31 October and then you will have extended lodgment dates (typically 15th May the following year but this can vary based on circumstance).

Company

A company’s tax is more complicated, and it is important to have an accountant like Beany to ensure you understand all the types of tax that could apply to your business. Some taxes are administered by the ATO and others are state-based taxes.

- Income tax for business – this is flat 25% if turnover is less than $50m annually

- Capital gains tax (CGT)

- Fringe benefits tax (FBT)

- Pay as you go (PAYG) withholding

- Pay as you go (PAYG) instalments

- Goods and Services Tax (GST)

- Fuel tax credits

- Wine equalisation tax

- Luxury car tax

- Payroll tax

- Land tax

In addition to taxes, you collect and pay, there are expenses you can claim to reduce your taxable income. When you do your tax return, you can claim most business expenses as tax deductions. See the ATO website for more information on tax deductions.

8. How do I know if my small business is going well?

Although you don’t need to know the nitty-gritty of accounting jargon, it’s useful to have a basic understanding when it comes to interpreting your financial statements. The three most important financial statements are balance sheet, profit and loss statement (income statement), and cash flow statement.

- Balance sheet provides a snapshot of the financial position of your business at a given point in time e.g. how much cash you have to how much you owe to suppliers.

- Profit and loss statement shows your business’ financial performance in a given period of time – this is effectively your net profit.

- Cash flow statement records incoming and outgoing cash of your business in a given period of time

Cloud accounting software such as Xero can provide some of the information you need. You can delve into the profit and loss statement and look at the key figures including sales (revenue), cost of sales, gross profit, non-cash expenses, operating expenses and net profit.

The cost of sales can increase if you hire an employee, for example. Your profit and loss statement should reflect an increase in sales or a reduction in your own workload.

Read more: Interpreting your profit and loss account

9. What happens if I want to exit my small business?

When starting a business, many people focus on initial setup and target markets, but it's wise to have a solid exit strategy, whether you're in it for the long haul or open to potential opportunities. You should discuss this with your accountant as they may have some recommendations on what you should look out for. These include appropriate structuring advice, how the owners are remunerated, and the way certain items are shown in the financial statements.

Bonus for the future entrepreneurs

At Beany, we have a starter pack designed to help kick-start your business. For $170 per month (for 1 year only), you can get:

- New business checklist and support: We will provide you with guidance and support on what you will need to do to establish and commence running your new business, including forming the company if you haven't already.

- Help setting up your business: we can provide advice on the best business structure for your needs and take care of establishment and registrations, making sure you're good to go.

- Xero setup and training: we can set up your Xero file so it is optimised for you and give you initial training so you can start off in the right way.

- Budgets prepared and input into Xero: preparation of a budget tailored to your business and input into your Xero file so you can track how you are going.

Contact us today and we’ll prepare you for growth.

Who are Beany?

We’re an online accounting firm that is always right here for you, your accounting pain relief. The most advanced technology lets us work way more closely with you than a normal accountant world.

We have a dedicated team of certified accountants and a support team to take care of your business no matter where you are, so you can focus on growing your business. We take out the ‘fluff’, break down the barriers and get things done. Looking out for you is what we are all about. Get started for free today.

Got any questions about Beany?

Chat to one of our friendly problem solvers today.

Tori Ma

Performance marketer

A performance marketing, and into true crime documentaries.

subscribe + learn

Beany Resources delivered straight to your inbox.

Beany Resources delivered straight to your inbox.

Share:

Related resources

Business structures – what’s best for you?

October, 2021Sole trader, partnership, and company are the common business structures in Australia. Making the right decision re...

How to start a business in Australia and get set for success

August, 2021Whether you’re an individual or entity looking to become an Australian tax resident, or you’re setting up a permane...

Spent money from a personal bank account?

July, 2021When you're starting out there can be a lot of set up in a short time. This can mean not all business expenses get ...