INDUSTRY NEWS • 3 APRIL 2024 • 1 MIN READ

GST regulation updates for businesses listing their services via a digital marketplace

New GST rules have been implemented from 1st April 2024 that impact businesses that utilise an online marketplace to sell or provide their service. For example, short-term accommodation providers like Airbnb, ridesharing services like Uber, and food delivery like Uber Eats.

What’s changed

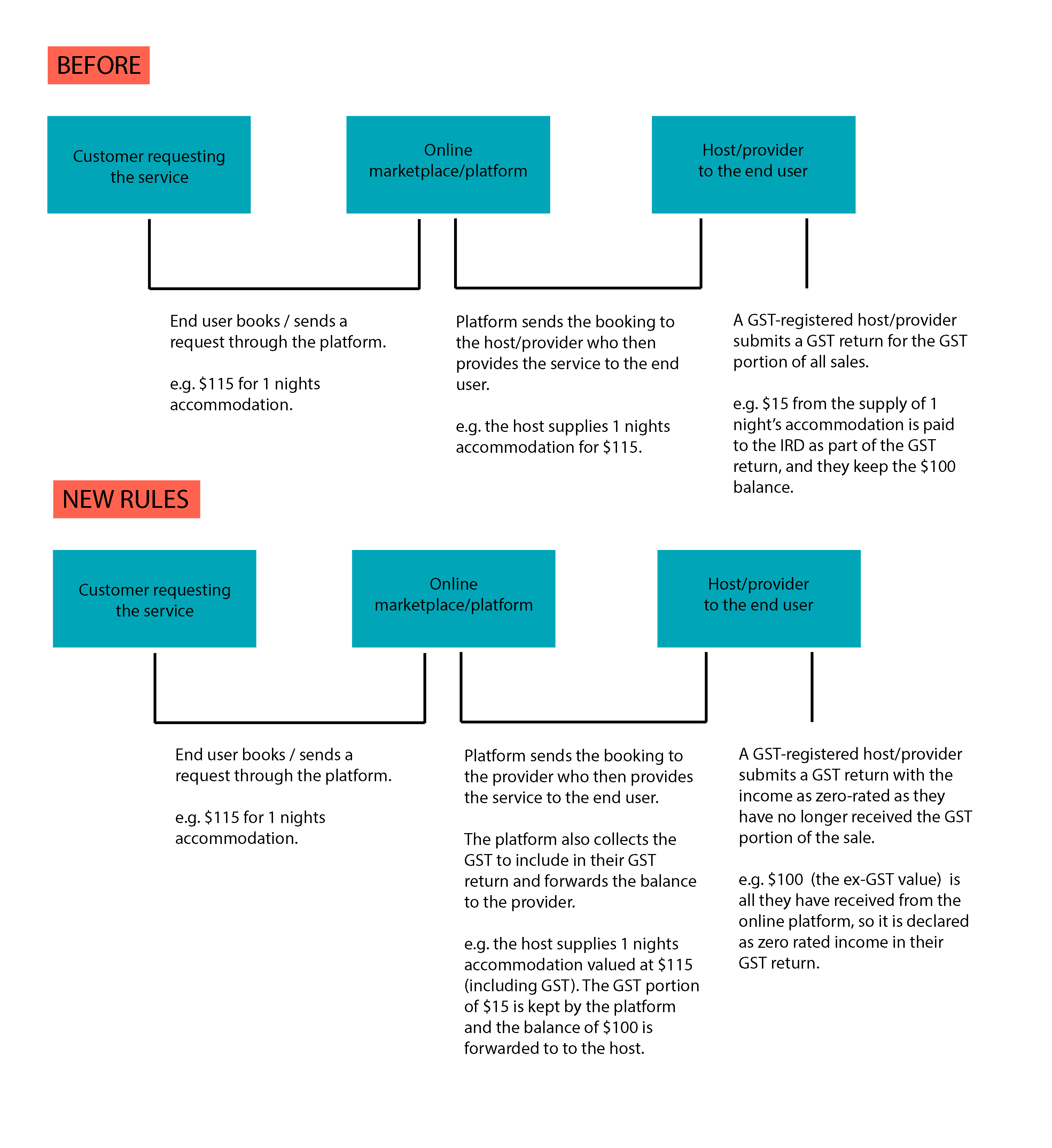

Under previous rules, end service providers (e.g. property owner or driver) who are GST-registered were responsible for collecting and returning GST to Inland Revenue for any provision of a service in New Zealand. Under the new rules, this is not the case.

Under the new rules, the electronic marketplace is responsible for collecting and returning GST to the IRD when a listed service on their platform is provided or received in New Zealand, regardless of whether the provider of the service is GST registered or not.

What this means if you use an online marketplace to sell your services and you’re GST registered

The new rules make it quite simple for you.

Since the digital platform that facilitates the sale of your service is now responsible for collecting and returning the GST on your behalf, payments you receive from the platform will be the ex-GST amount (use our GST calculator to get the GST exclusive price). This means that any income you earn via these platforms can be treated as zero-rated income in your GST returns. You can still claim the GST on any expenses like normal and if you have income that is earned from other means you still need to account for this as normal too.

What this means if you use an online marketplace to sell your services and you’re not GST registered

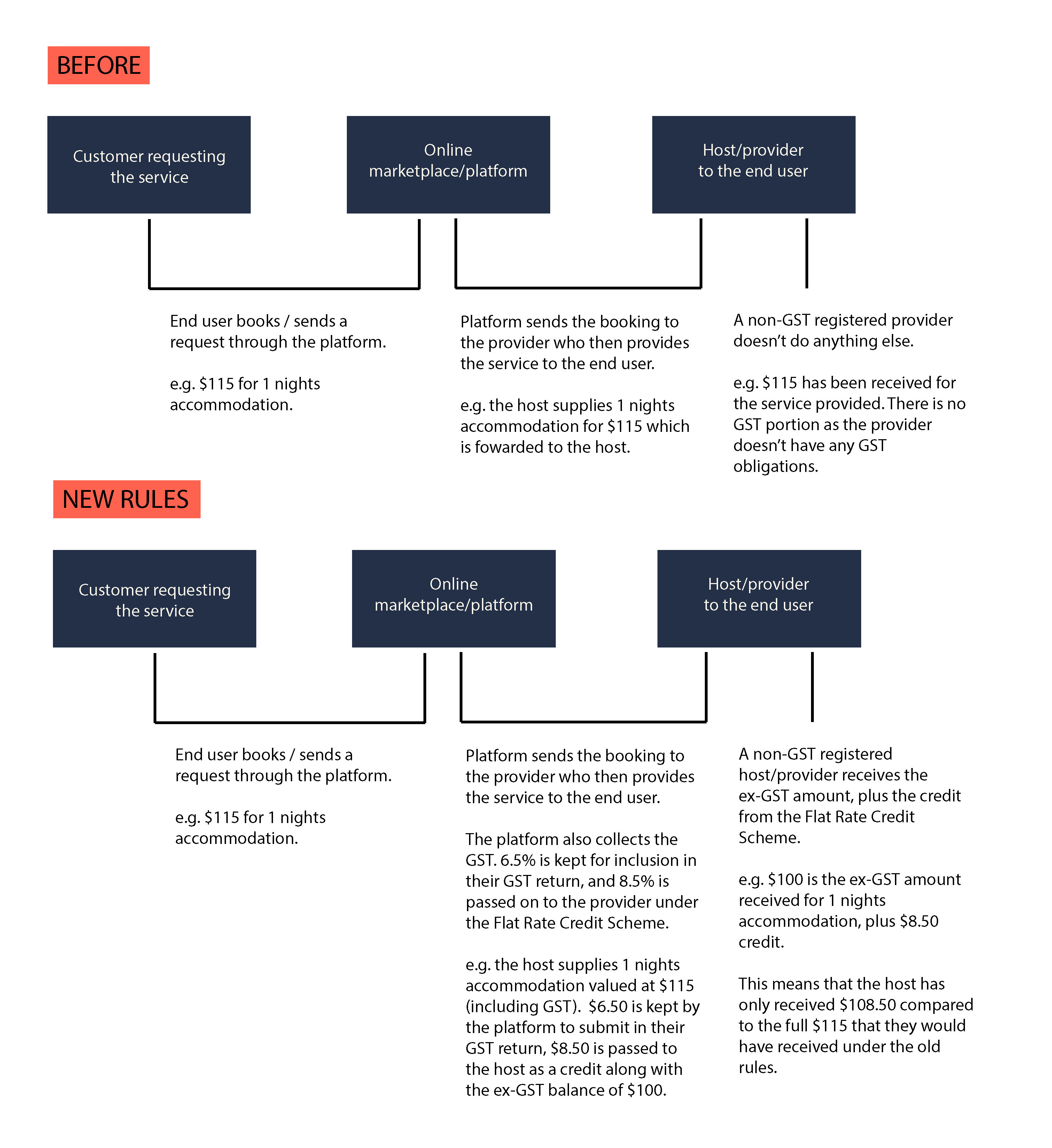

You can continue as normal. However, there are a few critical things you should be aware of.

With the changes, your pricing may be impacted if the listed prices are deemed inclusive of GST by the online marketplace. Since they now have to return GST on behalf of all providers on their platform, this will eat into your listed price. There is a credit scheme (see below), but these changes mean you will no longer receive the full amount of your listed price when a service is booked and provided.

Flat Rate Credit scheme

This credit scheme reduces the amount of GST that the marketplace has to return for non-GST registered providers.

Marketplace operators will still collect GST at 15% from your customer who has requested the service (i.e. the person who booked a stay at your accommodation, a driver or food delivery), but rather than returning the full 15% GST to the IRD, they only have to return 6.5%. The remaining 8.5% will be passed onto you as the end provider.

This 8.5% is intended to recognise the GST that unregistered sellers have on the costs for supplying the listed services.

Essentially, this means if you do not review or update your current pricing, you won’t be receiving the same net income as you used to due to the 6.5% being deducted from your list prices.

It’s important to note that if your total income is over $60,000 in a 12 month period, or goes over that amount, you will need to register for GST as normal and advise all platforms where you have your listings of the change so that they are aware to follow the rules for GST-providers instead.

Exemption

There is an opt-out available for large GST-registered accommodation hosts if they want to retain responsibility for collecting and returning their own GST.

The criteria for exemption is:

- Make more than NZ$500,000 in taxable supplies in a 12-month period; or

- Have more than 2,000 nights of accommodation listed on 1 electronic marketplace in a 12-month period).

Businesses who meet the first criteria can notify the online operator that they are opting out, but those who don’t make more than $500,000 but meet the 2000 night threshold must enter into an agreement with their operator to opt out.

What this means for marketplaces/platforms

The new rules make it more complicated from the platforms viewpoint as they now have to keep accurate information on all their suppliers and if they are GST registered or not.

We are already hearing of some platforms refusing to allow non-registered suppliers, or only working with those who are large enough to be exempt from the new rules.

Marketplaces/platforms will need a good accounting system and process in place to keep track of credit amounts for non-registered providers, and setting up bank rules in Xero to help with reconciling will be crucial.

Conclusion

In summary, if you’re a GST-registered service provider who uses a third party marketplace to facilitate the sale of your services, your life just got a bit easier.

If you’re non-GST registered, the main takeaway is to consider reviewing your prices so that you aren’t wearing the 6.5% that these platforms now need to pay on your behalf to the IRD.

If you operate an online platform or marketplace that facilitates the listing, sale and provision of services, then please consult with your accountant for some advice around the new rules and ensure your accounting software is optimised to do the heavy lifting.

Alaina Smith

Lead Accountant

Lives in the sunniest part of the country, running around after kids and the dog.

subscribe + learn

Beany Resources delivered straight to your inbox.

Beany Resources delivered straight to your inbox.

Share: