EXPENSES • 6 JUNE 2025 • 2 MIN READ

A guide to entertainment expenses

Back in corporate Australia in the 80’s, people were wining and dining staff and clients to “talk business” and claiming tax deductions under the umbrella that it was doing business. The government wasn't happy about it so they reformed the tax laws regarding entertainment and due to its nature and multiple scenarios, it’s one of the most complicated areas of tax law.

As a business owner, you know that entertainment expenses are an important part of your overall financial picture. Not only do they help keep your staff happy and increase their morale but it adds a positive culture to your business. But navigating the world of entertainment expenses can quickly lead you down a rabbit hole - what kind of expenses are tax-deductible, and which ones aren’t?

This guide will provide you with the information you need for entertainment expenses:

- What are entertainment expenses?

- Why, What, Where, When?

- What can you claim?

- FBT (Fringe Benefit Tax) implications

- GST on entertainment expenses

- Record keeping

What are entertainment expenses?

Entertainment can mean providing food, drinks and recreation. Recreation can include amusement, sport and similar leisure time activities e.g. tickets to sporting events, cruises, a joyflight or a harbour cruise.

It also includes accommodation or travel in connection with such entertainment above.

Some common examples of entertainment

- Christmas Parties

- Business lunches with clients

- Friday night socials

- Golf days

- Farewell and special celebration functions

- Corporate box functions

Entertainment expenses are generally not deductible (unless subject to FBT).

A couple of main exceptions need to be noted:

- Sustenance is not considered entertainment. For example, providing tea and coffee in the office for your staff is sustenance and not entertainment. Same with a few sandwiches given at a staff training session or morning or afternoon tea.

- Some entertainment is subject to FBT and if you pay FBT on an expense, then it is deductible for income tax. This is because FBT is already a tax on companies and the ATO doesn't want to give you a double kick of tax.

- Travel for business purposes

There are other exceptions listed in the Income Tax Assessment Act in s32-30 Employer expenses, s32-35 Seminar expenses, s32-40 Entertainment industry expenses, 32-45 Promotion and advertising expenses and s32-50 Other expenses. Many of these are complicated and require a whole article to explain.

If an expense is deductible for income tax, then you will be able to claim GST on that expense. The GST follows the deductibility of the expense.

Why, What, Where, When?

This heading might make you think of an inquisitive kid talking to you but actually, it’s a really good way to determine if an expense is considered entertainment. If you’re really keen for some bedtime reading, you can check out the details of these 4W’s in this tax ruling.

If you are providing food and drink to an employee, these four simple questions could be asked:

Why - Why was the food and drink provided? Were they just refreshments to complete the working day or was it provided to the employee to enjoy themselves?

What - What type of food and drink was it? Was the food pretty standard or was it fancy? Having alcohol as part of the equation points more towards entertainment than business.

Where - Food or drink provided on your business premises or at the employee's usual workplace is less likely to be entertainment. Food or drink provided off your business premises, such as at a function room, hotel, restaurant or consumed with other forms of entertainment, is more likely to be entertainment.

When - was it during the work day, during overtime or while an employee was travelling? If so, this is less likely to be entertainment.

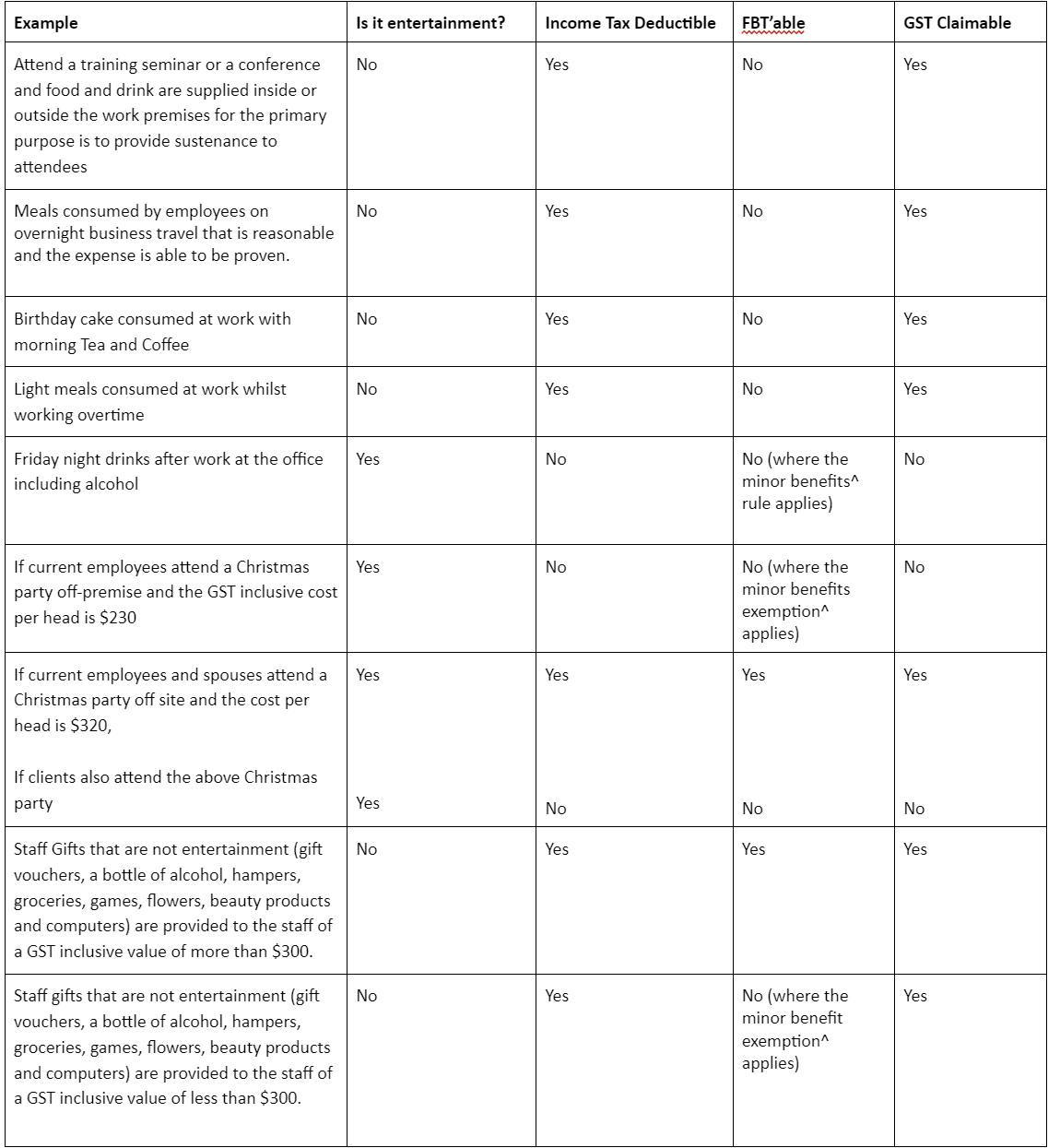

What can you claim?

The easiest way to give you an understanding of what is deductible can be done through common examples your business may face. This is not a comprehensive list but it gives you a starting point to think through how it works.

^ A minor benefit is one that is provided to an employee or their associate on an 'infrequent' or 'irregular' basis, which is not a reward for services, and at a cost less than $300 (inclusive of GST) per benefit. Read more about it from the ATO here.

Valuing entertainment benefits

Valuing entertainment benefits will affect the deductibility of expenses and GST claimability.

The Australian Tax Office (ATO) provides three methods that can be used by businesses to value and record their entertainment expenses:

1. Actual Method.

2. 50/50 Split Method.

3. 12 Week Register Method.

The Actual Method and the 50/50 Split Method are the most commonly used.

Actual Method

This method requires all entertainment benefits to be separated into the following categories:

- Client entertainment (inc GST)

- Staff entertainment

- Minor benefits less than $300 (inc GST)

Client entertainment is not tax-deductible and GST input tax credits cannot be claimed.

Meal entertainment provided to staff (and their associates) is subject to Fringe Benefit Tax. These costs will be tax-deductible and you are able to claim the GST input tax credits.

Minor benefits provided to staff (and their associates) are not tax-deductible and GST input tax credits cannot be claimed.

50/50 Split Method

The 50/50 Split Method is the easiest method to use. It takes the value of all meal entertainment provided (for staff, associates, clients and other persons) and treats 50% of the total as taxable entertainment.

Therefore, a tax deduction will be available and GST input tax credits can be claimed on the 50% subject to FBT. The other 50% is not deductible and GST input tax credits cannot be claimed.

The Minor Benefit Exemption does not apply if you choose this method.

Got any questions about Beany?

Chat to one of our friendly problem solvers today.

GST on entertainment expenses

GST can’t be claimed on non-deductible entertainment expenses. Only the GST portion of claimable entertainment expenses can be deducted.

For example, you’ve spent a total of $150 on books as gifts for your employees during April, May, and June. You’re eligible to claim the GST portion ($150/11 = $13.64) of your entertainment expenses at 100%. This is because the gifts are not entertainment.

Record keeping

You need to keep records such as invoices or receipts in order to make claims. As required by the ATO, you also need to keep records of the following information:

- The date you provided the entertainment

- Who is the recipient of the entertainment (are they an employee, associate of the employee or another person)

- The cost of the entertainment

- The kind of entertainment provided

- Where the entertainment is provided.

Who are Beany?

Beany are accountants for ambitious businesses, delivering big firm expertise without the big cost. We handle everything accounting-related (such as annual compliance, bookkeeping, financial insights and strategy), and help business owners make smarter decisions for their business and lifestyle through our responsive, friendly expertise. Book a call or get in touch if you want to discuss your business and see how we can help.

Ginette Chee

Accountant & Freelance Writer

Sydneysider Chartered Accountant who loves cooking, art and her Springer Spaniel Charlie.

subscribe + learn

Beany Resources delivered straight to your inbox.

Beany Resources delivered straight to your inbox.

Share:

Related resources

An expert guide on claiming business expenses

June, 2025Understand what you can and can't claim as business expenses in Australia.

Home office expenses: a tax deduction guide for business owners

June, 2025Learn how to claim home office expenses in Australia. Understand calculation methods, eligible deductions, and what...

7 top tips business owners should know to reduce your tax bills

October, 2022Many business expenses can be deducted from your income when calculating your tax bill. In simple terms, the lower ...