FINANCIAL LITERACY • 22 FEBRUARY 2021 • 3 MIN READ

Starting a cash flow forecast

In a previous blog, we explained the WHAT and WHY of preparing a cash flow forecast. The next step is HOW to prepare a forecast.

Profit and loss account

The first step is to run a Profit and Loss report in Xero on a monthly basis and get it to show comparatives for previous months. To do this, just follow these instructions, and then export the report to Excel. There – you have something in writing and a good starting point!

Next, critically review the income and expenses on a line-by-line basis and adjust each month up or down where needed. Don’t sweat the small stuff though!

- Your income may increase or decrease during holiday periods, or with the change in seasons

- Think about the timing of expenses

- Memberships may be once a year

- Superannuation Guarantee payments are made quarterly

- Your power bill is likely to be higher in winter

- Rates are paid four times a year

- Large planned maintenance costs should be included

- When will you sell purchased goods – the next month, the next season…?

- Do you pay less wages during the Christmas period?

- You may be considering extending your product range – how much additional revenue do you expect? How would your costs change?

- Maybe you’d like an additional employee – will this employee generate more business income, or perhaps take over some of your tasks to free you up? Remember – business improvement isn’t just about making money. Having downtime to enjoy your success is just as important

Balance sheet

Next, we add costs from outside of the Profit and Loss Account, month by month.

- Will you purchase assets, and when?

- Do you plan to sell an asset?

- Will you obtain a loan?

- Factor in any fixed loan or finance payments

- If you withdraw regular amounts from the business as living expense, include these as well

Tax stuff

Want to get even more tricky?

- Add your expected GST payments to each relevant month – include a formula which roughly calculates this from the information you’ve already entered

- If you know the amount of your provisional or terminal tax payments, add them in

- You can even estimate this, based on the figures in your Profit and Loss Account above

Please don’t be concerned if this is a little too technical for you. Remember – you just want to start the cash flow forecast. Tweaking it can come later.

Cash summary

The final step is to include separate rows for:

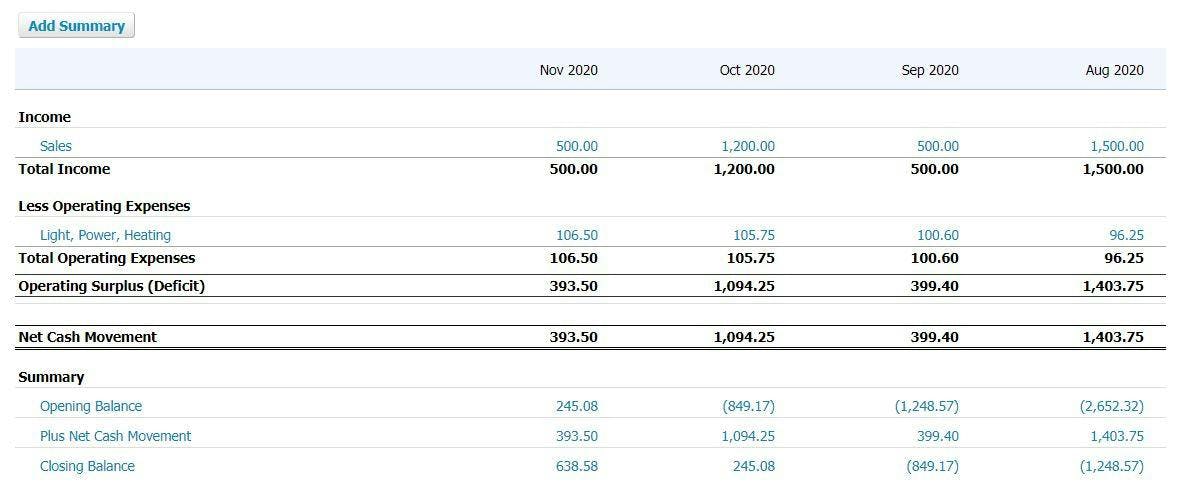

- The (expected) bank balance at the beginning of the forecast period – Aug 2020 in the snip below

- For the first month, you’ll need to type in the opening balance

($2,652.32) - For each of the following months, your opening balance will be the same as the closing balance from the previous month, so add a formula in your spreadsheet to cover that

Note how the opening balance for Sep 2020 is the same as the closing balance of Aug 2020 ($1,248.57) - The net cash movement for the month – this will be your income plus any money received from loans or sale of assets, minus expenses, minus payments for assets, taxes and loans

- $1,403.75

- The next row should have a formula, adding 1 and 2 together – this gives you your closing bank balance at the end of the month

- ($1,248.57)

Your cash flow forecast should look something like this:

What does your closing cash balance show you?

Now – if your formulas are working correctly, any change to any figures in any month will flow through to your forecasted closing cash balance.

- The monthly closing cash balances may indicate you need additional money- will you go into overdraft (with high interest rates) or find another funding source?

- Is there a build up of cash? What could you do with it – upgrade assets, wage increases, pay off debt, put aside for tax or savings?

- What would happen if you brought forward, or pushed back, the date you purchase an asset?

Who are Beany?

We’re an online accounting firm that is always right here for you, your accounting pain relief. The most advanced technology lets us work way more closely with you than a normal accountant world.

We have a dedicated team of certified accountants and a support team to take care of your business no matter where you are, so you can focus on growing your business. We take out the ‘fluff’, break down the barriers and get things done. Looking out for you is what we are all about. Get started for free today.

Got any questions about Beany?

Chat to one of our friendly problem solvers today to get clarity.

Kim Jenkins

subscribe + learn

Beany Resources delivered straight to your inbox.

Beany Resources delivered straight to your inbox.

Share:

Related resources

Why you should prepare a cash flow forecast

March, 2021A cash flow forecast is key to business sustainability and success. WHY? Many good businesses can be profitable, bu...

What is a cash flow forecast?

October, 2021Define what a cash flow forecast is and how it differs from a budget.