BUSINESS ADVICE • 14 NOVEMBER 2022 • 3 MIN READ

A simple guide on small business loan vs line of credit

As a business owner, you are impacted by many factors - seasonal fluctuations, lack of cash flow, faulty equipment or changing regulations could mean your business requires additional funding. This blog covers two options for funding - small business loans vs lines of credit.

Small business loans may already be familiar to you, but what about lines of credit? Here is a simple guide to the differences between these two finance options for you.

What is a small business loan?

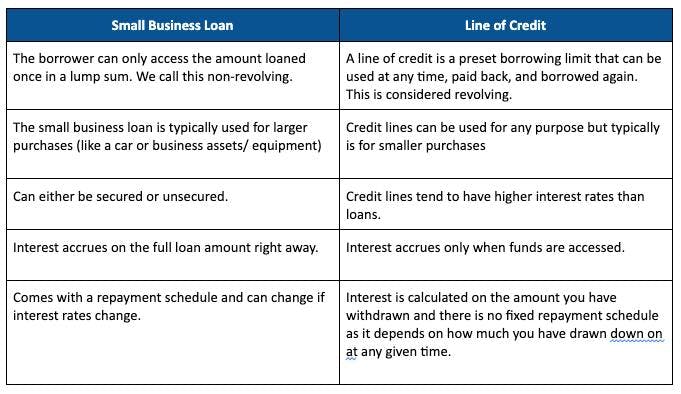

Small business loans are similar to personal loans, but for business purposes. It's a lump sum of money that you receive from your lenders.

As with personal loans, repayments and interest are scheduled for these loans. The total repayment amount is broken down into smaller repayments which are usually due on a regular basis (e.g., weekly, monthly). In essence, you have to pay the interest in addition to the amount borrowed throughout the loan term. Small business loan interest rates sometimes can vary, some lenders tailor their interest rates based on the business’s circumstances.

What is a line of credit?

Lines of credit work similarly to credit cards. In NZ, most major banks call their lines of credit product ‘revolving credit’. It means you can borrow money up to a credit limit and repay it over time. Once you’re approved to access a line of credit, you’ll be able to withdraw funds whenever it’s needed. Also, you only pay interest on the money you withdraw, not on the total amount available.

For example, if you have a $10,000 line of credit, you could withdraw $2,000 to purchase equipment for your business. You’ll only need to pay the interest on that $2,000, with the remaining $8,000 still available if needed.

Which one should I choose?

Now you’ve learnt the differences between a small business loan and a line of credit, you’ll want to decide what works best for you.

Here are some key questions to ask yourself before making your decision:

- What will be the amount you need and when do you need them?

- How much interest can you afford?

- What about your business’s financials? For example, how much revenue do you make each month? How long have you been in the business?

With these questions in mind, there are a few extra factors you should take into consideration when choosing a small business loan or a line of credit.

Amount needed

Small business loans generally offer a longer borrowing amount than lines of credit. If you need to purchase expensive business assets or equipment, it’s likely that a small business loan is better than a line of credit. However, if you need help with working capital or extra cash for meeting expenses for a short period, especially when expenses and income have yet to catch up to pay for employees’ salary or rent, a line of credit could be more appropriate.

Repayment plan

A major difference between a small business loan and a line of credit is that some lines of credit are revolving. The funds from the line of credit can be used up to your approved limit and repaid without having to reapply. A small business loan, on the other hand, is a lump sum you can borrow and repay once, with interest. If you run out of the borrowed money in your small business loan, you'll need to apply again.

In general, small business loans are best used for specific projects while lines of credits are more like business credit cards that you can use when you need it.

Predictability

You can apply for a business loan if you want a predictable payment schedule. By having a small business loan, you will have control over the repayment amount and period,and you can include those into your budget and forecast. On the other hand, the line of credit can be less predictable. You only repay it if you start to use the fund. It could good option if you have an inconsistent or unpredictable cash flow.

Who are Beany?

We’re an online accounting firm that is always right here for you, your accounting pain relief. The most advanced technology lets us work way more closely with you than a normal accountant world.

We have a dedicated team of certified accountants and a support team to take care of your business no matter where you are, so you can focus on growing your business. We take out the ‘fluff’, break down the barriers and get things done. Looking out for you is what we are all about. Get started for free today.

Tori Ma

Performance marketer

Performance marketer at Beany, and into true crime documentaries.

subscribe + learn

Beany Resources delivered straight to your inbox.

Beany Resources delivered straight to your inbox.

Share: