TAX • 19 AUGUST 2021 • 6 MIN READ

The basics business owners need to know about GST

GST (Goods and Services Tax) is a tax on most goods and services sold by businesses. While it feels like a tax on businesses, it really isn’t. Instead, it’s ultimately paid by people living out their day-to-day lives.

Businesses act like tax collectors for the government – charging an additional 10% on top of each sale, which they later forward to ATO.

A business’s process of reporting the GST to the government is called a Business Activity Statement (BAS).

When do businesses need to register for GST

We’ve got a whole article about that, over here. In summary:

If you’re earning over $75,000 per annum, you must register for GST.

If you’re earning under $75,000 per annum, GST registration is voluntary. It could be a beneficial move for you if

- You want to claim back GST on a large asset purchase, and you’re fairly sure your sales will be over $75,000 at some point

- Most of your sales are to overseas entities – you won’t collect GST on this income, but you can claim GST on the expenses you incur in Australia

For non-profit organisations where annual turnover exceeds $150,000 or if you're a taxi driver or ride-sharing driver (no matter your income), you will be required to register for GST.

Capturing your GST information – your GST basis

When you register for GST, you’ll need to select what’s called your GST basis. It’s how and when your GST records are entered into your BAS.

Your GST basis can be either:

- A Cash basis – Businesses with an aggregated turnover of less than $10 million can choose to account for their GST using the cash accounting method. Whenever cash is received into or paid from your bank account, your GST is entered into your BAS.

- A Non-Cash basis – your GST calculation is based on the dates of invoices you send and receive, rather than what goes through your bank account

The non-cash method is better suited to businesses that are not paid immediately.

Understanding a GST period

Quarterly – if your GST turnover is less than $20 million – and the ATO have not told you that you must report monthly.

Monthly – if your GST turnover is $20 million or more.

Annually – if you are voluntarily registered for GST and your GST turnover is under $75,000 ($150,000 for not-for-profit bodies).

Charging GST

Once you’re registered for GST, you can charge it. If you send out invoices for more than $82.50 (including GST), you need the following items:

- document is intended to be a tax invoice

- your (the seller’s) identity (Company name or your name)

- Your (the seller’s) Australian business number (ABN)

- date the invoice was issued

- brief description of the items sold, including the quantity (if applicable) and the price

- GST amount (if any) payable – this can be shown separately or, if the GST amount is exactly one-eleventh of the total price, as a statement which says 'Total price includes GST'

- extent to which each sale on the invoice is a taxable sale

If your invoices are over $1,000, you also need to include:

- The name and address of the buyer

- The quantity of whatever they have purchased, with the GST exclusive and inclusive amounts separately noted

If you’re using an accounting system for invoicing, it’s usually set up to capture all the information you need.

Got any questions about Beany?

Chat to one of our friendly problem solvers today to get clarity.

Claiming GST

You can claim GST on most transactions, and we’ll discuss in detail the situations when you can’t further down. Some of the transactions that commonly confuse business owners are outlined below.

GST can be claimed on the following

- Asset purchases

- You can claim GST on second-hand items even if the seller is not registered*

- You can claim GST upfront on assets purchased on finance

- GST can be claimed on the market values of existing assets you bring into the business

- Software providers

- Subscriptions to overseas providers such as Microsoft, Spotify, Facebook, Google AdWords etc can be claimed for GST

- Reimbursements to employees for business costs (including motor vehicle), but excluding mileage reimbursements

* If you claim GST on the purchase of second-hand assets, GST must be paid when it’s sold

GST on property transactions (including land) is a complex area and you need specialised advice before signing any documents

GST cannot be claimed on the following

- Transaction charges (known as financial services – which are all exempt from GST)

- Bank fees

- Interest expenses

- Stripe, Paypal (and similar) fees

- Loan fees

- Merchant fees

- Surcharge on credit card charges

- Donations

- Wages and salaries

- Goods purchased overseas (but you can claim any import duty charged by Customs)

- Penalties

- Loans and loan payments

- Sale of a business as a going concern

- Sales of investments such as shares, bonds and term deposits

- Payments to suppliers who are not registered for GST (except for second-hand assets as described above)

- Allowances paid to employees

- Residential rental expenses

- Personal expenses

For a more general application of what you cannot claim - refer to the ATO website here

GST and purchases for private use

If you purchase goods or services for both business and private use, you can only claim a GST credit for the part of the purchase relating to your business use.

If you later find your actual use differed from your intended use, you may need to adjust the amount of GST credits you have claimed.

If you are a small business, you may be able to account for the private portion of your business purchases once a year, rather than each time you lodge an activity statement. To do this you need to make an annual private apportionment election.

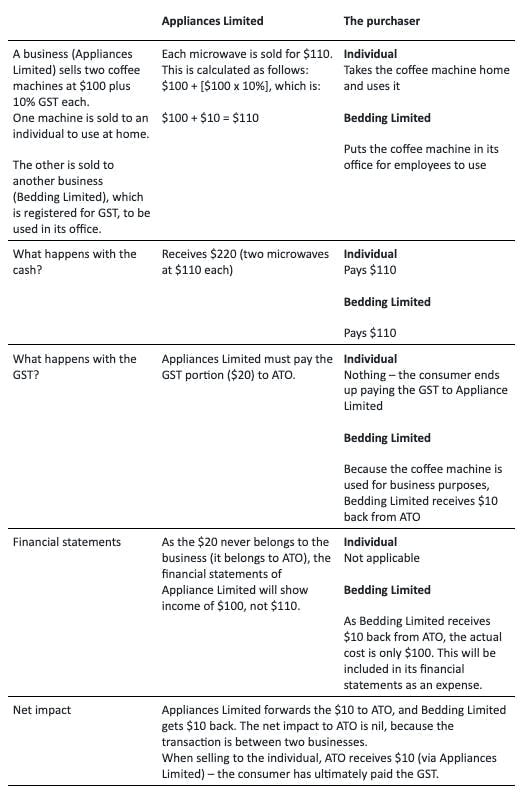

Example – comparing goods sold to a consumer and to a business

At the beginning of this post, we said that GST is ultimately paid by people living out their day-to-day lives. The example below shows how this happens.

Who are Beany?

We’re an online accounting firm that is always right here for you, your accounting pain relief. The most advanced technology lets us work way more closely with you than a normal accountant world.

We have a dedicated team of certified accountants and a support team to take care of your business no matter where you are, so you can focus on growing your business. We take out the ‘fluff’, break down the barriers and get things done. Looking out for you is what we are all about. Get started for free today.

Kim Jenkins

subscribe + learn

Beany Resources delivered straight to your inbox.

Beany Resources delivered straight to your inbox.

Share:

Related resources

ATO crack down on GST refunds

May, 2022Are you in an industry such as construction, agriculture or education that regularly receives GST refunds? If so, t...

How (and when) to register for GST

August, 2021GST is a tax on most goods and services in Australia. How does GST work? When should you register or deregister?