INDUSTRY NEWS • 21 MARCH 2021 • 8 MIN READ

What’s up with the new housing rules?

The Government has just announced a plan which it believes will help stabilise the housing market. First-time house buyers will be most benefited by these changes.

The significant changes are outlined further below but are by no means the complete list. If you are purchasing or settling the purchase of a residential rental property, or borrowing against a rental property, over the next week, there are many technicalities in the small print – please seek professional advice!

What are the most significant changes?

Residential rental property owners

- Interest on rental properties will no longer be allowed as a tax deduction – this is huge! Not many thought the Government would go down this path, but here it is

- Interest-only loans on rental properties may be limited, if not scrapped, in the future

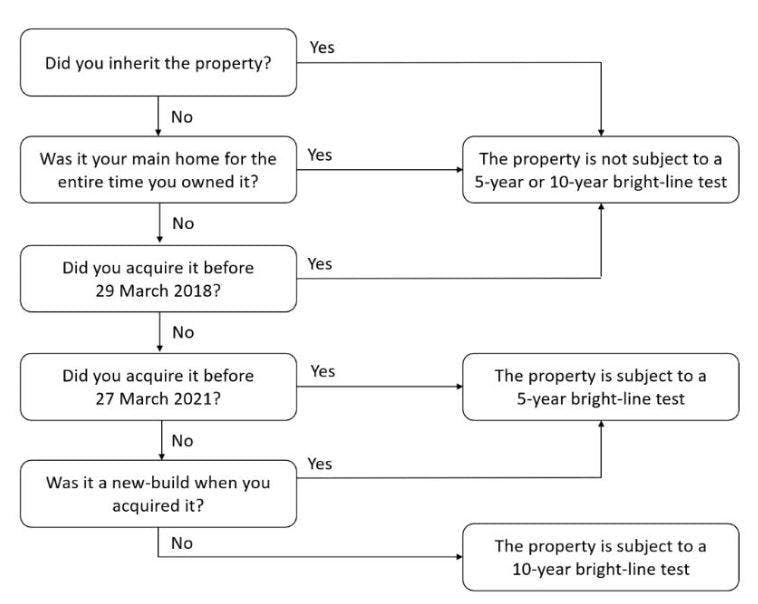

- The Brightline test will be extended to ten years (currently five), although new-build investment properties will still have five years

New home buyers

- First Home Grant Scheme (if you have contributed to Kiwisaver for at least three years)

- $5,000 per buyer if an existing property is purchased

- $10,000 per buyer for new-builds

- If you earn less than $95,000 as an individual, or $150,000 as a couple, you will now qualify for the First Home Grant

- scheme (previously $85,000 and $130,000)

- First Home Loan Scheme

- First-time buyers can borrow with a 5% deposit, instead of the more usual 20%

- If you earn less than $95,000 as an individual, or $150,000 as a couple, you will now qualify for the First Home Loan scheme (previously $85,000 and $130,000)

- The cap on the purchase price of the property increases by up to $100,000, depending on where you live and if it’s a new-build. This means that more properties will be available to first-home buyers seeking to borrow against a property – previously, you may have needed a 20% deposit, but if the property price is less than the new cap, you would only need 5%.

When do these rules start?

The Brightline test

For sale and purchase agreements that become unconditional on or before 27 March 2021, the “old” Brightline test is applied.

All other properties with a settlement date on or after 28 March 2021 will be subject to the revised Brightline test.

Interest deductibility

- Property purchased on or after 27 March 2021 – interest can be claimed up to and including 30 September 2021. After that, no interest can be claimed

- Property purchased on or before 26 March 2021 can claim the percentages outlined below

Are there any exemptions?

Yes.

- Your family home is not subject to any of the above rules

- Property developers can continue to deduct interest in full

- Commercial property owners can continue to deduct interest in full

Conclusion

These new rules will have caught many by surprise, particularly on the non-deductibility of interest. Add the fact there is less than five days’ notice for the legislation to take effect, and you have many residential rental property owners scrambling for information.

Nobody has all the answers yet. There is bound to be some fine-tuning and tweaking during the coming year as exemptions are clarified, but we cannot speculate on what these may be. We will update this post upon further announcements from the Government.

Who are Beany?

We’re an online accounting firm that is always right here for you, your accounting pain relief. The most advanced technology lets us work way more closely with you than a normal accountant would.

We have a dedicated team of remote accountants to take care of your business no matter where you are, so you can focus on growing your business. We take out the ‘fluff’, break down the barriers and get things done. Looking out for you is what we are all about. Get started for free today.

Got any questions about Beany?

Chat to one of our friendly problem solvers today to get clarity.

Kim Jenkins

subscribe + learn

Beany Resources delivered straight to your inbox.

Beany Resources delivered straight to your inbox.

Share:

Related resources

Airbnb income and how to handle it

December, 2021Tax on rental income in New Zealand can be complicated. We'll break down rules for income tax and GST whether it's ...

8 signs you should switch your business accountant

August, 2022Business owners sometimes shy away from the thought of switching business accountants even though there are some ob...

What’s included in a profit and loss account?

March, 2021We break down exactly what makes up a profit and loss account.