TAX • 24 FEBRUARY 2022 • 8 MIN READ

Residual vs Provisional vs Terminal taxes – confused?

If you’re not dealing with the subject every day, it’s difficult to understand, and you’re not alone!

We often find that when explaining types of taxes to clients, it seems logical and understandable. However, uncertainty creeps in later about why these taxes have different names.

Here’s a quick guide to the terminology.

- Summary

- Taxable Income (individuals)

- Tax on Taxable Income

- Tax Paid at Source

- Residual Income Tax

- Provisional Tax

- Terminal Tax

- Worked example

We always want to make things as clear as possible, but sometimes we can’t avoid using certain expressions. Our blog, What’s your accountant talking about? sets out simple explanations and gives examples of how we may use the phrases.

Summary

Let’s start from the end and work our way through the terms. There’s a worked example in the last section below.

- Tax on Taxable Income – the total tax you need to pay, based on your taxable income

- Residual Income Tax – tax to pay after deducting tax already paid by others on your behalf (for example, PAYE by employers and RWT by banks)

- Provisional Tax – tax paid in advance for the current year to reduce your terminal tax bill

- Terminal Tax – amount left for you to pay the IRD to clear the tax year

Taxable Income (individuals)

First up – we need to know how much overall tax you need to pay as an individual taxpayer. This is based on your taxable income, which can come from a number of sources. We see the following income sources most often, but the list isn’t exhaustive:

- Salaries and wages

- Schedular income

- Shareholder salary

- Business income (profit from your business if you’re a sole trader)

- Investment income

- Interest

- Dividends

- Government assistance

- Superannuation

From here, we can deduct certain expenses:

- Fees to prepare your personal tax return

- Income protection insurance (not health insurance)

The result is your Taxable Income.

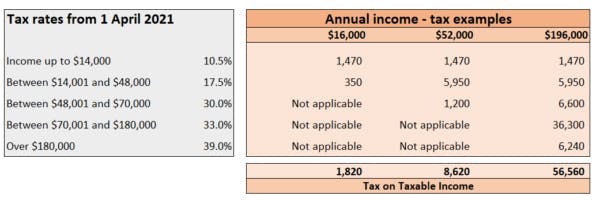

Tax on taxable income

Once we have your individual taxable income, we calculate the tax. Inland Revenue sets the tiers and percentages – we’ve included a few examples below.

And so, we arrive at your Tax on Taxable Income.

Dividend Withholding Tax (DWT)

When companies distribute dividends to its shareholders, they are required to distribute these at 33%. However, the company tax rate is currently 28%. So this extra 5% has to be payable as a top up by the company at the time it declares the dividend to the shareholders.

When you receive a dividend statement from a company or investment, you will notice there is usually always RWT and Imputation credits. This RWT is actually the dividend withholding tax – just to confuse you!

You can find out more about dividends in our blog – Dividends and Imputation Credits.

Provisional tax

If your Residual Income Tax (RIT) is higher than $5,000, you fall into the provisional tax regime.

This is probably the most difficult to get your head around. You’re thinking about the current tax year, but we’re asking you to pay tax for next year! We’re making sure you meet the Inland Revenue’s tax requirements and keeping any interest and penalties charged to the bare minimum – preferably nil.

What you’ve been (hopefully) doing, is paying the requested amounts to reduce your final 2022 tax payable to Inland Revenue.

Here’s where the timing gets confusing. For the 2022 tax year, your provisional tax payments will have been August 2021, January 2022, and May 2022. Your final tax bill for the 2022 year will be due in April 2023 or February 2023**.

For the 2023 tax year, we’ll be asking you to pay as follows:

- August 2022, January 2023, and May 2023*.

- The final wash-up (terminal tax) will be due in April 2024 or February 2024**

It feels like you’re paying tax all the time, and you probably are! We have a separate blog explaining the timing.

IRD requirements for provisional tax

The standard requirement is for the taxpayer to pay the prior year RIT (see further below) plus 5%. If that prior year return hasn’t been filed, they’ll go back to the year before that, plus 10%.

* Except if you prepare your GST returns every six months

** If you don’t have Extension of Time

Terminal tax

The remaining 2022 tax to pay on 7 April 2023 (or 7 February 2023) if you don’t have the Extension of Time). It’s your Total Tax to Pay less Tax Paid at Source (by others) less Provisional Tax (tax you’ve paid in advance for that income tax year).

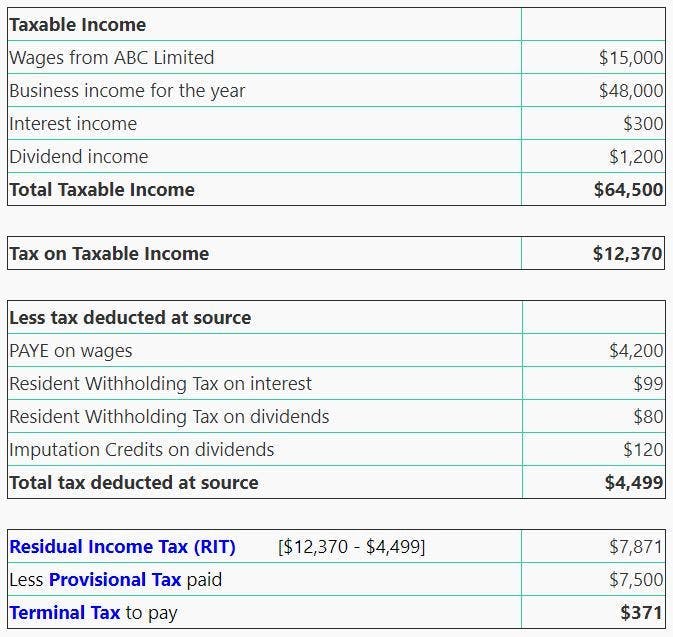

Worked example

How Beany can help?

We’re an online accounting firm that is always right here for you, your accounting pain relief. The most advanced technology lets us work way more closely with you than a normal accountant would.

We have a dedicated team of remote accountants to take care of your business no matter where you are, so you can focus on growing your business. We take out the ‘fluff’, break down the barriers and get things done. Looking out for you is what we are all about. Get started for free today.

Got any questions about Beany?

Chat to one of our friendly problem solvers today to get clarity.

Kim Jenkins

subscribe + learn

Beany Resources delivered straight to your inbox.

Beany Resources delivered straight to your inbox.

Share:

Related resources

Help us reduce your tax bill!

January, 2022We’re covering the Beany questionnaire, some tax tips, and a brief look at changes in 2022 laws which could impact ...

6.7% discount on tax!*

February, 2021In certain circumstances, you can get a 6.7% tax discount from the IRD on your provisional tax.

Home office expenses: a tax deduction guide for business owners

September, 2022Whether you're a business owner, freelancer, or contractor, you could claim home office expenses related to busines...