FINANCIAL LITERACY • 23 FEBRUARY 2021 • 5 MIN READ

How does a shareholder current account work?

If you have a company structure*, you’ll probably see the line item ‘Shareholder Current Account’ in the balance sheet. It’s one of the most difficult concepts to understand, so we prepared the blog ‘What is a Shareholder Current Account?‘

This article is to show you how it works in practice.

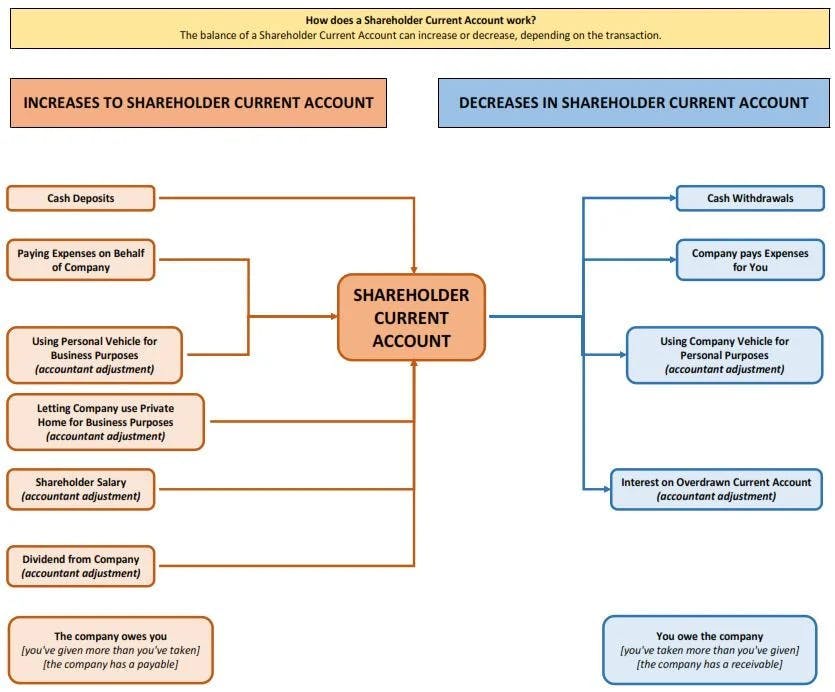

The diagram below shows examples of how the shareholder current account can increase and decrease. The components are explained after the diagram. There’s also an example towards the end, so you can see how it all falls into place.

You want to have a positive shareholder current account, where the company owes you money – that is, the company has a liability to you.

* A trust can have a Beneficiary Current Account, which is similar in nature.

Increases and decreases

Cash transactions

The first two transactions on each side are straight forward as they involve movement in the company’s bank account.

- You deposit money into the company to get it going or boost it, and/or you pay company expenses yourself. This increases your shareholder current account – Funds Introduced or Cash Deposits

- You withdraw money out of the company to live on, and/or the company pays for your personal expenses. This reduces your shareholder current account – Drawings

Accountant’s adjustments

Our aim is for you to pay the least amount of tax legally possible. We therefore make adjustments as we prepare the company’s financial statements.

Shareholder salary

At the end of the year, Beany looks at the profit of the company. This is calculated as all the income less all the claimable expenses. Now – somebody needs to pay tax on that profit.

As you probably have a lower tax rate than the company, Beany may allocate a salary to you out of the profit – the amount will depend on personal attribution rules*, and the market rate salary. All this means is that we move (part of) the profit from the company to you. No cash changes hands, so the company still owes you that salary. The balance of your shareholder current account increases. This is the Shareholder Salary and we include this figure in your personal tax return.

* Personal attribution rules are Inland Revenue’s way to combat those who operate as a company (28% tax rate), rather than as a sole trader (up to 39%) purely for tax purposes.

Motor vehicles

The company may make one or more of its vehicles available to you for personal use. If it does, this is a benefit for you – you don’t need to purchase your own car, the company pays for insurance, maintenance, fuel, etc. You need to reimburse the company for this benefit. Again, no cash changes hands. We calculate the amount and call this a Motor Vehicle Reimbursement – it’s considered to be company income. In your shareholder current account, this may be a separate line item, or we may include it in Drawings. Your current account decreases.

In some instances, you may let the company use your personal vehicle. The company needs to reimburse you for this because you’re paying for the insurance, maintenance, etc. We make a calculation to determine the amount. The company includes this within Motor Vehicle Expenses in the Profit and Loss Account. The company doesn’t physically pay you, so this increases the amount it owes you – it increases your shareholder current account. We usually include the transaction within Funds Introduced.

Home office expenses

These days, a lot of people work from home and/or use it to do the book-keeping side of the business – raising invoices, paying suppliers, reconciling bank accounts, using the internet, and making phone calls.

Instead of the company having to rent office space itself, you provide part of your home as an office. You need to give us information about the office size, interest paid on a mortgage, rent, power, rates, etc. We calculate what the company should pay for this privilege and included as a Home Office Expense in the company’s Profit and Loss Account. Again, as no cash changes hands, the company owes you this money and it increases your shareholder current account. We include this within Funds Introduced or show as a separate line item.

Negative shareholder current account

If you take from the company more than you give, you will hear the words ‘you have an overdrawn current account’ – you owe the balance to the company. From the company’s perspective, it’s given a loan to the shareholder. In the normal course of business, if the loan was to a third party, the company would charge interest. Because of this, the company is legally required to charge you interest on the overdrawn amount

We perform our calculations based on IRD rates and show it as Interest on Overdrawn Shareholder Current Account (income for the company) in the Statement of Profit and Loss, and in your Shareholder Current Account.

An overdrawn current account is almost always a warning sign of pressure so, if you hear this, take it seriously and make time to understand what’s going on.

In the unlikely event that the company folds and you have an overdrawn current account, Inland Revenue may consider it to be a dividend and you’d pay tax on this.

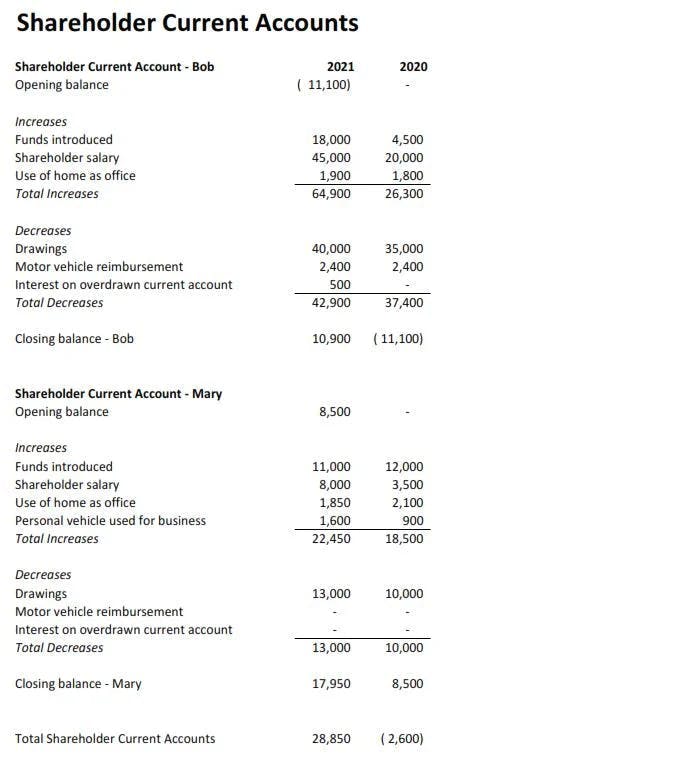

Example

This is what you may see in your financial statements – a separate page headed Shareholder Current Accounts.

Who are Beany?

We’re an online accounting firm that is always right here for you, your accounting pain relief. The most advanced technology lets us work way more closely with you than a normal accountant world.

We have a dedicated team of certified accountants and a support team to take care of your business no matter where you are, so you can focus on growing your business. We take out the ‘fluff’, break down the barriers and get things done. Looking out for you is what we are all about. Get started for free today.

Got any questions about Beany?

Chat to one of our friendly problem solvers today to get clarity.

Kim Jenkins

subscribe + learn

Beany Resources delivered straight to your inbox.

Beany Resources delivered straight to your inbox.

Share:

Related resources

What is a shareholder current account?

February, 2020The shareholder current account is used to keep track of the money you contribute to the business and all the money...